Our CFO, Chris James, shares key insights and a simple action plan, as recent budget changes will start to affect property investors and savers as we approach the end of the tax year on 5th April.

Tax changes

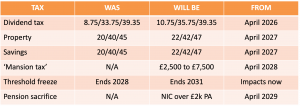

The Budget on 26th November made tough reading for those receiving income outside of traditional PAYE models. A whole range of measures was announced, but their impact was spread over several tax years:

If you have dividend income from a source you can control, then see the Action Plan section below.

Making tax digital (MTD)

As well as changes to rates and thresholds, individual property investors and the self-employed also have significant potential impacts on how they administer their taxation affairs, perhaps as soon as next month for some.

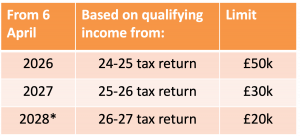

If you personally own property or have sole trader income, you need to know your ‘qualifying income’, which is broadly your income from this activity each year before expenses. If this value is over £50k per annum, you will likely need to comply with the MTD rules, which require quarterly filing of information and digital record-keeping. If your income is lower than this, you may have to comply in future years:

*Announced at Budget November 2025

Action plan for dividends and MTD

If you think you may be subject to the MTD rules, based on your ‘qualifying income’, speak to your accountant or tax advisor now, who should be able to help you with a solution.

If you have dividend income and can control the timing of dividend payments, you need to consider whether to take action before the tax year ends on the 5th April. The basic and higher rates of dividend tax increase from 6 April 2026, but the additional rate remains unchanged. As a result of this, you may wish to accelerate dividends to pay them before the end of the tax year.

Example: You normally take £50k in dividends per tax year. If you know you will need an extra £50k this summer, say, for a wedding or property deposit, you could take an extra dividend in July**, when it would likely fall into the higher rate band and be taxed at 35.75%. However, if you take the extra £50k dividend now, you will be taxed at the current higher dividend rate of 33.75% instead, saving you £1,000.

**Remember that a dividend taken earlier will mean tax is payable sooner, as it will appear on an earlier tax return. You can only pay dividends from distributable reserves. If you’re not sure how that works, speak to your accountant.

NB: Your personal taxation treatment will depend on your individual circumstances – do take personalised advice from a suitable advisor before taking any action.

About

Chris James is the Chief Financial Officer at Inflow Group, a specialist finance provider to the property sector. He is a recently qualified Chartered Manager and Fellow of the CMI, holding a postgraduate diploma in Strategic Management. He has a background as a Chartered Accountant in practice environments, with broad experience in the SME sector. During his time in the recruitment sector, he regularly met with HMRC, the Treasury, OTS, EASI and other bodies to discuss tax and employment rights. He also has experience as a non-executive board member and Chairperson.